Jonathan van den Berg · May 20, 2026

Trump Bank Citizenship Executive Order: How Banks Could Soon Check Your Status and What It Means for Global Finance

A senior U.S. official once described unchecked financial flows as “the lifeblood of illicit networks that threaten both security and economic stability.” President Trump’s new executive order directing banks to verify clients’ citizenship status aims to cut off that blood supply, marking the latest move in a long-running battle over who gets access to the world’s most important financial system.

“The lifeblood of illicit networks that threaten both security and economic stability runs through our financial institutions. We are turning off the tap.”

That blunt assessment, delivered by a senior Treasury official last year, captures the thinking behind President Trump’s new executive order on bank citizenship checks. Signed in May 2026, the directive instructs federal regulators to guide banks on verifying the citizenship or immigration status of customers when they open accounts or conduct significant transactions. The goal is straightforward: stop money tied to illegal immigration, sanctions evasion, and other cross-border crimes from moving freely through American banks.

This is not a small tweak. U.S. banks handle roughly $2.5 trillion in cross-border payments every day. Even modest changes in how they screen customers can ripple across global markets, affecting everything from remittances sent by workers abroad to investment flows from emerging economies. The order lands at a moment when banks already face pressure from sanctions on Russia, Iran, and certain Chinese entities, plus growing worries about cryptocurrency’s role in moving money outside traditional oversight.

Cryptocurrency Trading and the Erosion of the Petrodollar has shown how blockchain tools let people sidestep banks entirely. The new citizenship rule tries to close one door even as technology opens others.

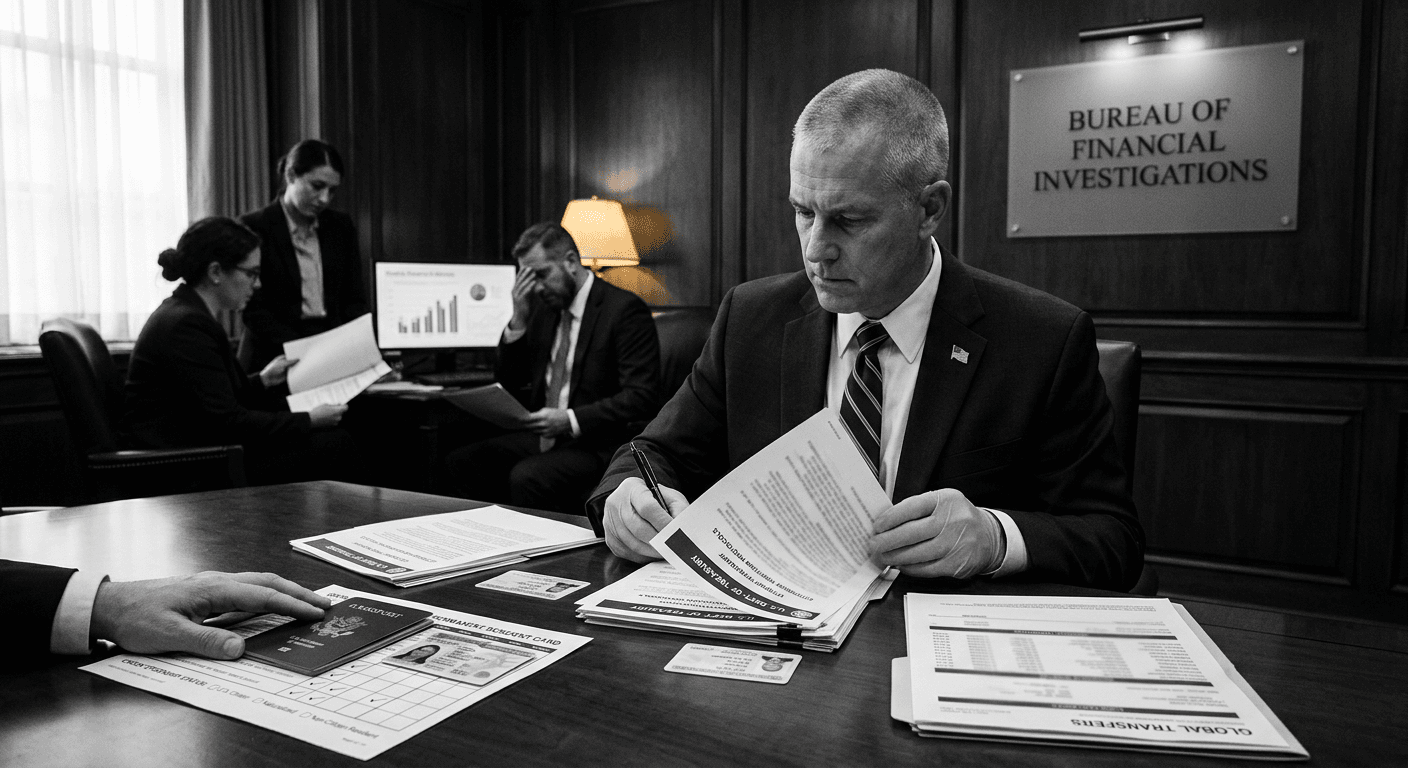

What the Order Actually Requires

The executive order does not create a new federal database of every bank customer. Instead, it directs agencies including the Federal Reserve, the Office of the Comptroller of the Currency, and the Financial Crimes Enforcement Network (FinCEN) to issue guidance within 90 days. Banks must incorporate citizenship and lawful-presence checks into their existing “know your customer” (KYC) processes.

For most consumers this will feel like one more form. Banks already collect Social Security numbers, addresses, and tax IDs. The new step adds verification against immigration records for non-citizens. Large transfers, business accounts, and certain investment products will face tighter scrutiny. Banks that fail to comply risk losing access to federal deposit insurance or facing higher regulatory costs.

Critics worry this will push people without full documentation toward unregulated financial channels. Supporters argue the opposite: forcing money into the regulated system makes it easier to track illicit flows. Early estimates from banking industry groups suggest compliance could cost mid-sized banks between $50 million and $200 million each in the first two years, mainly for updated software and staff training.

The Economic and Security Rationale

Proponents tie the order to two big problems. First, remittances and cash transfers sometimes help finance activities the U.S. considers security risks. Second, lax account-opening rules have allegedly let people living illegally in the United States build credit, buy property, and move money in ways that undermine immigration law.

Data from the World Bank shows migrant remittances to Latin America and South Asia topped $800 billion globally in 2025. A significant slice passes through U.S. banks or money-service businesses. The new rules aim to ensure that only those legally present can use the formal banking system for large or repeated transfers.

At the same time, the order strengthens tools already used for sanctions enforcement. Banks have spent billions since 2010 building compliance departments to block transactions tied to Iran, North Korea, and Russian oligarchs. Adding citizenship checks fits into that infrastructure. It treats immigration status as another red flag, similar to how banks currently flag transactions from certain countries.

This connects directly to broader energy and security concerns. Gas Prices and the Strait of Hormuz illustrate how tightly financial sanctions, energy flows, and global prices are linked. Cutting off access to dollar-based banking remains one of the most powerful non-military tools available.

Impact on Banks and Markets

Wall Street reacted with cautious acceptance. Shares of major banks dipped slightly on news of the order but recovered quickly. Analysts expect large institutions like JPMorgan Chase and Bank of America to absorb the costs more easily than regional lenders. Smaller banks that serve immigrant communities could face harder choices: invest in compliance or risk losing certain customer segments.

The order also touches on the ongoing tension between financial inclusion and security. For years policymakers pushed banks to serve more unbanked people. Now the emphasis has shifted toward verifying legal status first. This mirrors debates in Europe, where banks must navigate both EU anti-money laundering rules and national immigration policies.

International implications are significant. Foreign nationals with legal visas or green cards will likely see smoother processes once systems are updated. Those without status may turn to cash-based systems, informal hawala networks, or crypto platforms. The latter trend links to Bitcoin ATMs Face Crackdown as Crypto Challenges Traditional Finance, where regulators already worry about anonymous wealth transfers.

Reactions from Different Corners

Immigrant advocacy groups called the move discriminatory and likely to hurt families sending money home for food, school, and medical care. Banking trade associations asked for clear rules and sufficient time to implement changes without disrupting everyday business. Privacy advocates raised questions about how citizenship data will be stored and shared between banks and government agencies.

On the other side, national security analysts welcomed the focus on “beneficial ownership” and real identity. They point to cases where shell companies and lax KYC allowed sanctioned individuals to move money through U.S. accounts. The new emphasis on citizenship is seen as a logical extension of post-9/11 reforms that first required banks to know their customers.

Some economists warn of unintended consequences. If millions of people lose easy access to banking, overall economic activity in certain sectors could shrink. Construction, agriculture, and service industries that rely heavily on immigrant labor might feel knock-on effects if workers cannot easily cash checks or receive electronic payments.

Global Context and Parallel Moves

The United States is not acting alone. The European Union has tightened its anti-money laundering directives in recent years, including stricter rules on who can open accounts. China monitors capital outflows aggressively. Even crypto-friendly jurisdictions like Singapore and the UAE now require more identity verification for digital asset firms.

What makes the U.S. move distinctive is its explicit link between immigration enforcement and financial access. By treating lawful presence as a core compliance issue, the order blurs the line between domestic policy and international financial regulation. This matters because the dollar remains the world’s reserve currency. Access to dollar clearing affects trade, investment, and even humanitarian aid worldwide.

The timing also matters. Global markets face uncertainty from trade tensions, energy price swings, and rapid technological change in finance. In this environment, clearer rules on who can participate in the formal system can reduce some risks even as they create others. Investors watching stock market volatility already understand that policy clarity, even when controversial, can eventually stabilize expectations.

Related shifts appear in other areas of economic statecraft. From semiconductor supply chains to energy politics, governments increasingly use access to their markets and financial systems as strategic tools. This citizenship order fits that pattern.

What Happens Next

Regulators must now produce detailed guidance. Banks will update policies, train staff, and invest in technology that can quickly check status without slowing down routine transactions. FinCEN is expected to expand its list of red-flag indicators to include patterns common in unauthorized immigration-related banking.

Legal challenges are likely. Lawsuits will test whether the executive branch can direct banks to collect and act on immigration data this way. Courts will weigh national security and financial integrity arguments against claims of overreach and discrimination.

For ordinary people the practical outcome will depend on implementation. Citizens and legal residents should notice little change beyond perhaps one extra question during account opening. Undocumented individuals and some mixed-status families may find certain services harder to obtain. Money-transfer companies that serve immigrant communities will need to adapt or risk losing market share to less regulated channels.

Longer term, the order could accelerate two trends: greater use of digital identity technologies and further growth in parallel financial systems outside traditional banks. Both developments carry their own risks and opportunities.

Why This Matters for Everyday Economic Life

Most people do not think much about the plumbing of the global financial system until it affects their paycheck, mortgage, or ability to send money to family. This executive order reaches into that plumbing. It says that in the world’s most important financial market, legal status now sits alongside credit scores, tax compliance, and sanctions lists as a factor institutions must consider.

Whether this ultimately makes the system safer, fairer, or simply more bureaucratic remains to be seen. What is clear is that financial access is never neutral. Every rule about who can open an account, send a wire, or take a loan shapes who can fully participate in the modern economy.

The Trump administration bets that tightening the rules on citizenship will reduce illegal activity and strengthen enforcement of existing immigration law. Critics counter that the costs to families, small businesses, and economic dynamism will outweigh the gains. Both sides agree that the dollar’s central role gives the United States unusual leverage. How that leverage is used will continue to shape global finance for years to come.

In the end, this debate is about more than banks checking documents. It is about the balance between security and openness in an interconnected world where money, people, and power cross borders constantly. Getting that balance right affects inflation trends, investment flows, energy markets, and the daily economic prospects of millions. The new citizenship checks are one more tool in that larger effort.

Conclusion

President Trump’s executive order on bank citizenship verification reflects a clear priority: use the power of the U.S. financial system to enforce immigration and security rules more effectively. While the full effects will unfold over months and years, the direction is set. Banks will collect more data. Regulators will watch more closely. And the debate over who belongs inside the formal financial tent will grow louder.

Smart observers will watch three things: how smoothly banks implement the guidance, whether illicit flows actually decrease, and how people adapt when formal banking becomes harder to access. Those outcomes will determine whether this policy strengthens American financial security or simply pushes problems into the shadows of cash, crypto, and offshore systems.

Either way, the conversation about money, borders, and power just became more concrete. In a world of volatile markets, energy tensions, and rapid technological change, concrete rules may be exactly what many participants have been waiting for.

Share This Article