Jonathan van den Berg · June 1, 2026

Bitcoin ATMs Face Crackdown: How Scams and Regulation Are Reshaping Crypto's Challenge to Traditional Finance

Bitcoin ATMs have become flashpoints for fraud, prompting lawsuits, bankruptcies, and stricter rules. This crackdown highlights the tension between crypto's promise of financial freedom and regulators' efforts to curb criminal use while traditional banks maintain control.

Bitcoin ATMs are under growing regulatory pressure as scams multiply and governments tighten controls. Operators face lawsuits alleging they enabled massive impersonation fraud, while one major player filed for bankruptcy amid new state-level rules designed to stop criminals from exploiting the machines.

The crackdown reflects deeper tensions: crypto's challenge to traditional finance collides with authorities' determination to prevent money laundering, fraud, and sanctions evasion. For everyday users, this means higher fees, stricter verification, and fewer convenient locations. For the industry, it raises questions about whether Bitcoin ATMs can survive as a bridge between cash and digital assets or if they will become another regulated financial service.

Key Takeaways

- Bitcoin Depot faces a class-action lawsuit claiming its ATMs enabled over $76,000 in impersonation scams targeting elderly victims.

- A retired Florida couple is suing the company directly after losing significant savings through fraudulent transactions.

- At least one major Bitcoin ATM operator filed for bankruptcy as Florida introduced stricter licensing and compliance requirements.

- Global regulators, including those following FATF guidelines, are increasing scrutiny on crypto ATMs for anti-money laundering compliance.

- Despite setbacks, the Bitcoin ATM market continues expanding in regions with lighter regulation, highlighting uneven global enforcement.

- The battles over Bitcoin ATMs mirror broader geopolitical struggles over who controls access to financial systems in an increasingly digital world.

The Rise of Bitcoin ATMs and Their Economic Role

Bitcoin ATMs allow users to buy or sell cryptocurrency using cash or cards without needing a bank account. This feature made them popular in underbanked communities and among people wary of traditional financial institutions. By 2026, thousands of machines operate worldwide, processing billions in annual volume.

The appeal is simplicity. Insert cash, scan a wallet QR code, and receive Bitcoin. Some machines also support selling crypto for cash. This bypasses many layers of traditional banking, offering speed and privacy that appeals to privacy advocates and those in countries with unstable currencies.

Economically, these machines serve as on-ramps for retail crypto adoption. They lower barriers for first-time buyers who distrust exchanges or lack digital payment methods. In places with limited banking infrastructure, Bitcoin ATMs function almost like informal remittance services, echoing how cryptocurrency trading challenges the petrodollar system.

Major Lawsuits Targeting Bitcoin ATM Operators

The most prominent legal action involves Bitcoin Depot. A class-action lawsuit alleges the company's machines facilitated impersonation scams totaling at least $76,000. Scammers reportedly posed as government officials or tech support, convincing victims to buy Bitcoin at the machines and send it to fraudsters.

According to court filings, operators failed to implement adequate safeguards despite knowing about the pattern of fraud. Victims, often elderly, lost life savings in minutes. The suit claims Bitcoin Depot profited from high transaction fees while turning a blind eye to obvious red flags.

In a separate case, a retired Florida couple sued Bitcoin Depot directly after falling victim to a similar scam. The couple reportedly lost tens of thousands of dollars after a caller convinced them to use a local Bitcoin ATM. Their lawsuit argues the company has inadequate anti-fraud measures and profits from transactions that should have been blocked.

These cases are not isolated. Similar lawsuits have targeted other operators, accusing them of enabling drug trafficking, ransomware payments, and sanctions evasion. The pattern suggests Bitcoin ATMs have become a favored tool for criminals seeking quick, hard-to-trace conversions between cash and crypto.

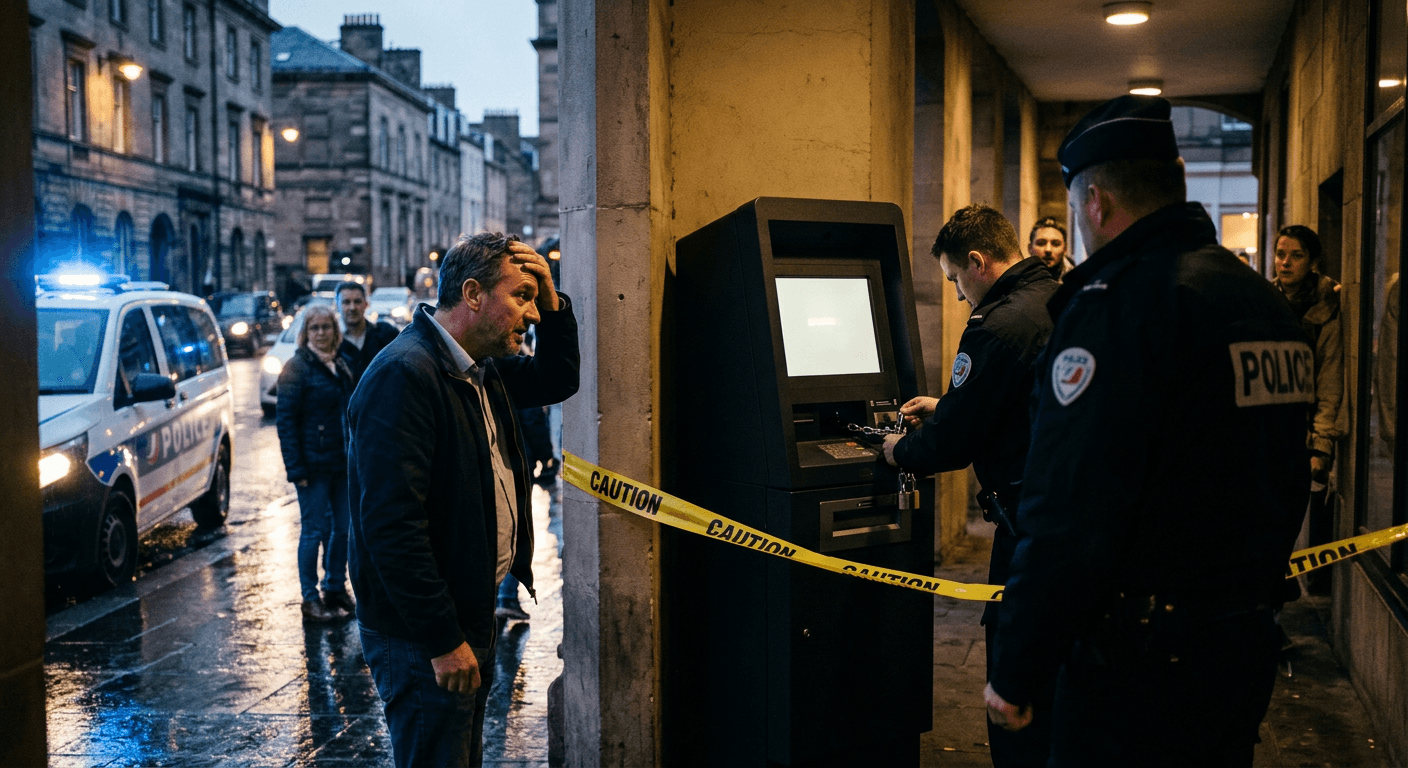

Bankruptcy and Florida's Regulatory Crackdown

The pressure became too much for at least one operator. A prominent Bitcoin ATM company filed for bankruptcy as Florida tightened rules aimed at preventing fraud. The new requirements include enhanced licensing, mandatory transaction monitoring, and stricter customer identification protocols.

Florida's move reflects a national trend. States increasingly view Bitcoin ATMs as money transmitters requiring robust compliance programs. Operators must now verify customer identities more thoroughly, report suspicious activity, and sometimes limit transaction amounts.

These rules raise operating costs significantly. Smaller operators struggle to absorb compliance expenses, while larger firms invest in sophisticated monitoring software. The result is industry consolidation, with only well-capitalized companies likely to survive the new environment.

The bankruptcy highlights a harsh reality: what began as a decentralized, permissionless technology now faces the same regulatory burdens as traditional financial services. This shift directly challenges crypto's original promise of operating outside legacy banking systems.

Global Regulatory Response and Geopolitical Dimensions

Regulators worldwide are aligning on tighter standards for virtual asset service providers, including Bitcoin ATM operators. The Financial Action Task Force (FATF) updated guidelines urge countries to treat crypto ATMs like any other money service business, requiring registration, record-keeping, and suspicious transaction reporting.

In the United States, federal agencies coordinate with states on enforcement. European regulators have taken similar steps, with some countries requiring physical presence and enhanced due diligence for operators. This coordinated pressure reflects growing concern that unregulated crypto channels could undermine sanctions regimes and enable cross-border crime.

The geopolitical angle is clear. As nations compete for economic influence, control over financial rails becomes strategic. Bitcoin ATMs represent a potential bypass around SWIFT and traditional banking networks. Governments wary of losing monetary sovereignty push back hard. This mirrors concerns raised in discussions around how Bitcoin reshapes global financial power structures.

Meanwhile, authoritarian regimes sometimes tolerate or even encourage crypto channels when they help evade Western sanctions. The uneven global enforcement creates arbitrage opportunities but also increases risks for legitimate users caught in the regulatory crossfire.

How Bitcoin ATMs Enable Scams: Common Tactics

Understanding the fraud patterns helps explain the regulatory backlash. Impersonation scams dominate Bitcoin ATM crime. Perpetrators contact victims by phone, email, or text, claiming to be from the IRS, a bank, or tech support. They create urgency, instructing victims to buy Bitcoin immediately to "secure" funds or avoid penalties.

Once victims reach an ATM, scammers stay on the phone providing step-by-step instructions. The speed of the transaction leaves little time for second thoughts. Because Bitcoin transactions are irreversible, funds disappear quickly once transferred to the scammer's wallet.

Other tactics include:

- Romance scams: Fraudsters build online relationships then invent emergencies requiring Bitcoin payments.

- Investment fraud: Fake crypto platforms direct users to ATMs to "fund" nonexistent accounts.

- Tech support scams: Attackers claim a computer is compromised and demand Bitcoin paid via ATM.

High fees—often 10-20% per transaction—make these machines particularly attractive to criminals. The cash-based nature also appeals to those avoiding digital trails.

Impact on Legitimate Users and Crypto Adoption

The crackdown creates friction for honest customers. Many Bitcoin ATMs now require government ID, selfie verification, or transaction limits. What once took seconds now involves several minutes of compliance steps. Fees have risen as operators pass on compliance costs.

Locations are disappearing in heavily regulated markets. Users in rural areas or those without easy access to exchanges face fewer options. This particularly affects unbanked populations who benefited most from the technology.

Yet the industry adapts. Some operators invest in better compliance technology, including AI-driven fraud detection. Others focus on business-to-business services or partner with regulated financial institutions. The surviving machines may become more trustworthy even as they lose some of their original decentralized character.

This evolution parallels broader trends in crypto where innovation collides with institutional requirements. The Ethereum Foundation's strategic adjustments demonstrate how even core projects recalibrate in response to regulatory and market realities.

Common Mistakes When Using Bitcoin ATMs

- Sharing wallet details or seed phrases with anyone claiming to provide assistance.

- Using machines in high-crime or poorly lit areas where criminals may observe transactions.

- Believing urgent phone calls demanding immediate Bitcoin purchases without independent verification.

- Ignoring transaction fees that can exceed 15%, making small purchases uneconomical.

- Failing to research the specific operator's reputation and complaint history before using a machine.

- Not using privacy features like TOR or non-custodial wallets when possible.

Best Practices for Safe Bitcoin ATM Use

- Verify independently. Never act on instructions from unsolicited calls or messages. Contact organizations directly using official numbers.

- Start small. Test the machine and process with a minimal amount before committing larger sums.

- Choose reputable operators. Look for machines from established companies with transparent policies and clear fee disclosure.

- Protect your privacy. Use a fresh wallet address for each transaction. Consider using privacy-focused coins or mixers where legally permitted.

- Document everything. Take photos of the machine, receipt, and transaction details in case of disputes.

- Enable security features. Use machines with video surveillance and good lighting when possible.

- Understand local regulations. Know the reporting thresholds and compliance requirements in your jurisdiction.

The Future of Bitcoin ATMs in a Regulated World

Bitcoin ATMs will likely survive but in evolved form. Expect continued consolidation as only compliant, well-funded operators remain. Technology improvements—biometric verification, real-time blockchain monitoring, and integration with regulated exchanges—will make machines harder to abuse while maintaining accessibility.

The broader question involves crypto's place in global finance. As traditional institutions adopt blockchain technology and central banks explore digital currencies, the need for cash-to-crypto on-ramps may diminish. Yet in regions with capital controls, unstable banking systems, or limited digital infrastructure, Bitcoin ATMs will retain their appeal.

The tension between innovation and control continues. Crypto's challenge to traditional finance forces regulators to adapt while pushing the industry toward greater professionalism. How governments balance these forces will determine whether Bitcoin ATMs remain tools of financial inclusion or become heavily regulated relics of crypto's wilder early days.

FAQ

Are Bitcoin ATMs legal?

Yes, in most jurisdictions, but they face increasing regulation. Many areas require operators to register as money transmitters, implement anti-money laundering programs, and comply with know-your-customer rules. Always check local laws before using one.

Why are governments cracking down on Bitcoin ATMs?

Authorities cite their use in scams, money laundering, ransomware, and sanctions evasion. The cash-based, relatively anonymous nature makes them attractive to criminals. Regulators want stronger customer verification and transaction monitoring to reduce illicit activity.

How can I avoid scams at Bitcoin ATMs?

Never buy Bitcoin in response to unsolicited calls, emails, or texts. Verify any claimed emergency independently. Use only reputable operators, start with small test transactions, and protect your wallet information. If something feels wrong, walk away.

Do Bitcoin ATMs report transactions to the government?

Many operators must file currency transaction reports for amounts above certain thresholds, typically $10,000 in the US. Suspicious activity reports may be filed regardless of amount if fraud or illegal behavior is suspected. Compliance requirements vary by country and operator.

Will Bitcoin ATMs disappear because of regulation?

Unlikely. While some locations close and smaller operators exit, demand for easy cash-to-crypto conversion remains strong. The industry is consolidating around compliant operators who use advanced technology to meet regulatory requirements while serving legitimate customers.

How do Bitcoin ATMs make money?

Operators charge substantial fees, typically between 7% and 20% per transaction. Some also earn from the spread between buy and sell prices. High fees help cover compliance costs, machine maintenance, and cash handling expenses.

Further reading on this site:

The Erosion of the Petrodollar and Cryptocurrency’s Strategic Crossroads

Share This Article