The Inner Path · April 14, 2026

Croatia’s Path to the Eurozone Core: Economic Convergence, Energy Politics, and Geopolitical Realignment in Southeast Europe

As Croatia solidifies its position inside the Eurozone and Schengen, the country has become a bellwether for how smaller EU member states navigate energy security, fiscal discipline, and great-power competition between Brussels, Washington, and Beijing in an increasingly fragmented global order.

On 1 January 2023, Croatia became the 20th member of the Eurozone, replacing the kuna with the euro and completing a remarkable 30-year journey from the ruins of the Yugoslav wars to full monetary integration with Europe’s core economies. By April 2026, the country’s economic and geopolitical significance has only grown. Amid global energy shocks, supply-chain reconfiguration, and rising tensions between the United States, the European Union, and an assertive China, Croatia finds itself at the intersection of several strategic vectors: Balkan stability, Mediterranean energy politics, EU fiscal governance, and NATO’s eastern flank.

While trending today largely due to tourism announcements, sporting successes, and regional diplomacy, Croatia’s deeper story is one of economic convergence, prudent macroeconomic management, and a deliberate repositioning within the European and transatlantic architecture. This article examines the country’s economic performance since euro adoption, its role in regional energy security, the challenges of maintaining competitiveness inside a currency union, and the broader geopolitical implications for Southeast Europe.

Economic Performance and Convergence Since Euro Adoption

Croatia’s entry into the Eurozone was not merely symbolic. It followed strict compliance with the Maastricht criteria, including a budget deficit below 3% of GDP, public debt sustainably trending downward, inflation within reference values, and long-term interest rates aligned with the euro area average. By late 2022, public debt stood at approximately 68% of GDP, down from a post-pandemic peak above 85%. Inflation, while elevated in 2022–2023 due to the energy crisis, was brought back under control faster than in several larger Eurozone members.

In 2025, Croatia recorded real GDP growth of 3.1%, outperforming the Eurozone average of 1.4%. Tourism, which accounts for roughly 20% of GDP, rebounded strongly after the pandemic, with 2025 visitor numbers exceeding 22 million. More importantly, the country has made progress in diversifying its economy. Foreign direct investment (FDI) inflows reached €3.2 billion in 2025, with notable greenfield projects in renewable energy, advanced manufacturing, and information technology.

The European Central Bank’s monetary policy now directly shapes Croatian borrowing costs. The ECB’s rate-hiking cycle in 2022–2023 initially caused pain, with mortgage rates rising from under 2.5% to above 5%. However, the country’s conservative banking sector—largely foreign-owned by Italian, Austrian, and French institutions—avoided the worst excesses seen in other peripheral economies during previous cycles. Non-performing loans remain below 4%, a significant achievement.

Fiscal Discipline and the EU’s New Economic Governance Framework

Croatia has emerged as a quiet advocate for fiscal prudence within the EU. In negotiations over the revised Stability and Growth Pact and the new fiscal rules implemented in 2024–2025, Zagreb aligned itself with the “frugal” northern states rather than the high-debt southern bloc. This positioning reflects both political choice and economic necessity: with public debt still hovering near 60% of GDP in early 2026, Croatia understands that credibility in bond markets is essential for a small open economy inside a currency union without its own central bank.

The country has benefited from substantial EU recovery and cohesion funds. By April 2026, Croatia had absorbed over 85% of its €6.3 billion allocation under the Recovery and Resilience Facility. These funds have been directed toward green transition, digitalization, and infrastructure—particularly modernizing ports in Rijeka and Ploče to serve as logistics hubs for Central Europe’s access to the Adriatic.

Energy Politics and the Geopolitical Importance of Southeast Europe

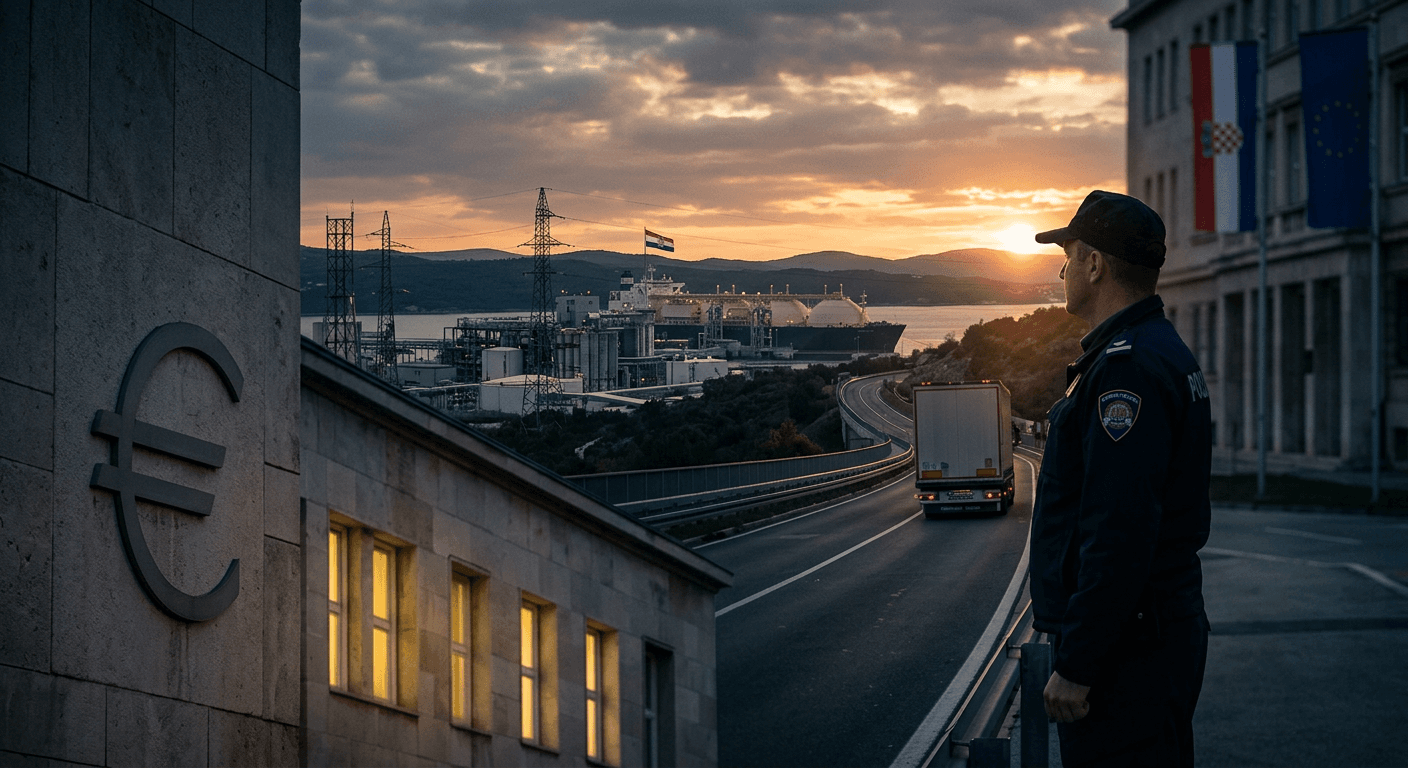

Energy security has become Croatia’s most strategically significant policy domain. The country sits at the crossroads of several major infrastructure projects that directly challenge Russia’s historical dominance over European gas markets and China’s growing influence in critical infrastructure.

The liquefied natural gas (LNG) terminal on the island of Krk, expanded in 2022–2024, now has a regasification capacity of 6.1 billion cubic meters per year. In 2025, the terminal supplied gas not only to Croatia but also to Hungary, Slovenia, Austria, and even parts of Ukraine via reverse flows. This diversification has reduced Southeast Europe’s dependence on Russian pipeline gas by an estimated 35–40% compared to 2021 levels.

Croatia is also central to the EU’s Southern Gas Corridor strategy. The Ionian-Adriatic Pipeline (IAP), designed to connect with the Trans Adriatic Pipeline (TAP), would bring Azerbaijani and potentially Turkmen gas into the Western Balkans. Political negotiations accelerated in 2024–2025 as the EU sought to accelerate its REPowerEU plan following Russia’s full-scale invasion of Ukraine.

The China Factor: Ports, Rail, and Strategic Autonomy

Beijing has not been idle. China’s COSCO has significant interests in the port of Piraeus (Greece) and has expressed interest in Rijeka and Trieste. Croatia has walked a careful line—accepting Chinese investment in non-critical sectors while blocking participation in sensitive infrastructure under EU foreign investment screening mechanisms strengthened since 2020.

The Pelješac Bridge, completed in 2022 with EU funding rather than Chinese loans, was a deliberate geopolitical statement. By choosing European contractors over cheaper Chinese bids, Croatia signaled its preference for Western alignment even at higher cost. This decision stands in contrast to Montenegro’s experience with the Chinese-financed Bar-Boljare motorway, which created a debt trap and required EU intervention.

In 2025, Croatia joined the EU’s Critical Raw Materials Club and began exploring lithium and rare earth potential in cooperation with German and Swedish firms. This reflects a broader European strategy of “friend-shoring” critical supply chains away from both Russia and China.

Regional Stability and the Western Balkans

Croatia’s geopolitical weight extends beyond its borders. As the most developed economy in the Western Balkans and a full EU and NATO member, Zagreb plays a crucial mentoring and stabilizing role for the remaining non-EU states in the region—particularly Bosnia and Herzegovina, Montenegro, and Serbia.

Croatia has been a strong advocate for EU enlargement, arguing that further delay risks opening the door to Russian and Chinese influence operations. In 2025, Zagreb supported granting candidate status to Bosnia once electoral reforms were implemented and pushed for accelerated accession talks with Albania and North Macedonia.

However, relations with Serbia remain complex. While economic cooperation has improved—bilateral trade exceeded €2.8 billion in 2025—political mistrust persists over war crimes legacies, minority rights, and Kosovo. Croatia’s firm support for Kosovo’s integration into international institutions continues to irritate Belgrade.

Migration, Demography, and Labor Markets

Like many Central and Eastern European countries, Croatia faces severe demographic challenges. The population has declined from 4.5 million in 1991 to approximately 3.85 million in 2026. Net emigration, particularly of young skilled workers, remains a drag on long-term growth potential despite recent positive net migration trends driven by returning citizens and inflows from Asia and Latin America.

The government has responded with pro-natalist policies, tax incentives for families, and active labor market policies aimed at attracting foreign workers, particularly in tourism, construction, and IT. Unemployment stood at 5.8% in early 2026, near historic lows, but labor shortages in specific sectors are acute.

Semiconductor Ambitions and the “Nearshoring” Opportunity

One of the more ambitious elements of Croatia’s economic strategy involves positioning itself within Europe’s semiconductor and advanced manufacturing supply chains. In partnership with the European Chips Act, Croatia has attracted investment from mid-tier suppliers in electronics and automotive components. While it lacks the scale for leading-edge foundries, its political stability, EU membership, relatively competitive wages, and improving education outcomes in STEM fields make it attractive for assembly, testing, and specialized materials production.

This strategy aligns with broader Western efforts to reduce dependence on Taiwan and mainland China for critical technologies. Croatia’s geographic position also makes it a potential node in the emerging “Middle Corridor” trade route connecting Europe with Central Asia, bypassing traditional routes vulnerable to Russian or Chinese disruption.

Challenges and Risks

Despite notable successes, Croatia faces structural headwinds. Productivity growth lags behind the Eurozone average. The economy remains overly dependent on tourism and seasonal employment. Public administration reform has been slow, and corruption perceptions, while improved, still rank below Nordic and Baltic peers according to Transparency International’s 2025 index.

Climate change poses an existential threat to its tourism model. Rising sea levels, heatwaves, and increasingly frequent “bora” wind extremes threaten both infrastructure and the Mediterranean climate that attracts visitors. The government’s National Climate and Energy Plan commits to 42% renewable energy by 2030, but implementation has been uneven outside of large hydro projects.

Geopolitically, any resurgence of Russian influence in Serbia or Bosnia, or a renewed migrant crisis on the Balkan route, could quickly destabilize the region. Croatia’s border with Bosnia remains a sensitive point in EU migration management.

Conclusion: A Model for Small-State Strategy in a Fragmenting World

Croatia’s experience since independence offers important lessons for other small and medium-sized powers. Through consistent Euro-Atlantic alignment, fiscal conservatism, strategic infrastructure investment, and pragmatic regional diplomacy, the country has transformed itself from a post-conflict state into a credible member of Europe’s economic and security core.

In an era of deglobalization, friend-shoring, and great-power competition, Croatia demonstrates that sovereignty and prosperity are not contradictory but mutually reinforcing when paired with credible institutions and clear strategic priorities. Its success in energy diversification, prudent management inside the Eurozone, and careful navigation of relations with larger powers offers a blueprint for other aspiring EU members in the Western Balkans.

As the European Union itself faces internal fragmentation and external pressure from Washington, Beijing, and Moscow, countries like Croatia—stable, Atlanticist, fiscally responsible, and strategically located—may prove more valuable to the bloc’s cohesion than their size suggests. The next decade will test whether Zagreb can translate these advantages into higher sustainable growth, deeper regional integration, and genuine convergence with Western European living standards.

The quiet Croatian success story deserves far more attention in international economic and geopolitical analysis than it typically receives. In 2026, as Europe rethinks its security and economic architecture, Croatia stands as both a beneficiary and a shaper of the new order taking shape on the continent.

Share This Article